Code

\[ \newcommand\ov{\overline} \newcommand\un{\underline} \newcommand\BB{\mathbb} \newcommand\EE{\mathbb{E}} \newcommand\mc{\mathcal} \newcommand\ti{\tilde} \newcommand\h{\hat} \newcommand\beq{\begin{equation}} \newcommand\eeq{\end{equation}} \newcommand\barr{\begin{array}} \newcommand\earr{\end{array}} \newcommand\bfp{\mathbf{p}} \newcommand\independent{\protect\mathpalette{\protect\independenT}{\perp}} \def\independenT#1#2{\mathrel{\rlap{$#1#2$}\mkern2mu{#1#2}}} \]

Everything we do boils down to population and sample mean

\((y_{i},x_{i,1},x_{i,2},...,x_{i,K})\) is random vector for \(i\)th observation from sample of size \(N\)

\[\EE\left[\left[\begin{array}{c}y_{1}\\\vdots\\y_{N}\end{array}\right]\Big| \left[\begin{array}{c}\mathbf{x}_{1}\\\vdots\\\mathbf{x}_{N}\end{array}\right] \right] = \left[\begin{array}{c}\mathbf{x}_{1}\mathbf{\beta}\\\vdots\\\mathbf{x}_{N}\mathbf{\beta}\end{array}\right]\]

\[ \EE[\mathbf{Y}|\mathbf{X}] = \mathbf{X}\mathbf{\beta} \]

Define \[ \epsilon_{i} = y_{i} - \EE[y_{i}|\mathbf{x}_{i}] \]

then by definition: \[ y_{i} = \mathbf{x}_{i}\beta + \epsilon_{i}\]

and \[ \EE[\epsilon_{i}|\mathbf{x}_{i}] = 0 \]

Let’s prove:

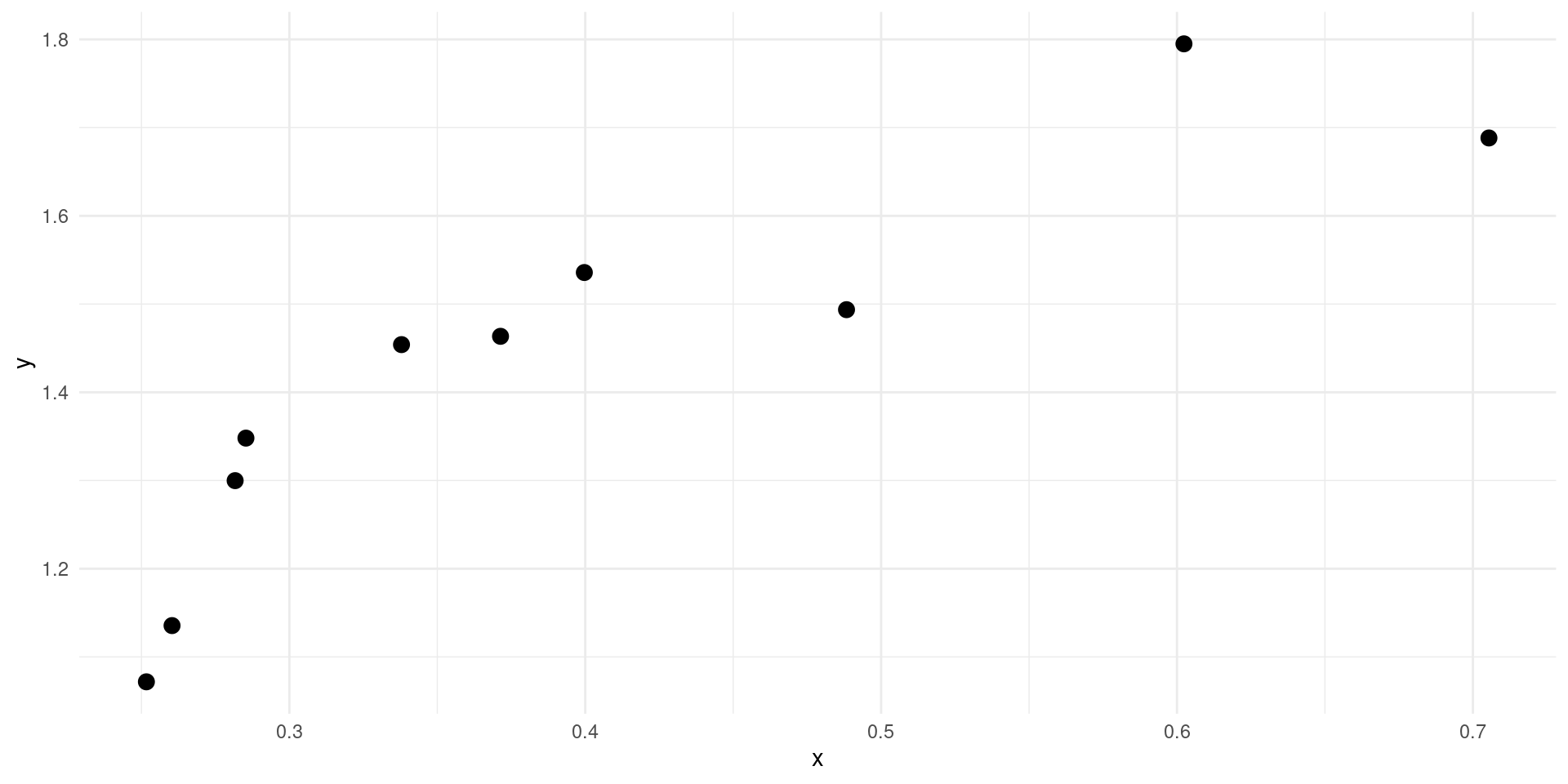

R using lm

Call:

lm(formula = y ~ x, data = d)

Residuals:

Min 1Q Median 3Q Max

-0.16941 -0.09998 0.04211 0.09441 0.10608

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.9199 0.1046 8.795 2.19e-05 ***

x 1.2767 0.2463 5.182 0.00084 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.1143 on 8 degrees of freedom

Multiple R-squared: 0.7705, Adjusted R-squared: 0.7418

F-statistic: 26.86 on 1 and 8 DF, p-value: 0.0008402Let’s verify that this uses the OLS formula

\[\EE\left[\hat{{\beta}}\right] = {\beta}\]

\[ \BB{V}\left[\hat{{\beta}}\right] = \frac{1}{N}\EE\left[\mathbf{x}_{i}^{T}\mathbf{x}_{i}\right]^{-1}\EE\left[\mathbf{x}_{i}^{T}\mathbf{x}_{i}\epsilon^2_{i}\right]\EE\left[\mathbf{x}_{i}^{T}\mathbf{x}_{i}\right]^{-1} \]

Homoskedasticity (\(\EE[\epsilon^2|\mathbf{x}]=\sigma_{\epsilon}^2\)):

\[\BB{V}\left[\hat{{\beta}}\right] = \frac{1}{N}\EE\left[\mathbf{x}_{i}^{T}\mathbf{x}_{i}\right]^{-1}\sigma^2_{\epsilon} \]

\[\hat{{\beta}} \rightarrow_{d} \mc{N}\left({\beta},\BB{V}\left(\hat{{\beta}}\right)\right)\]

\[\hat{{\beta}} = (\mathbf{X}^{T}\mathbf{X})^{-1}\mathbf{X}^{T}\mathbf{Y}\] \[\widehat{\BB{V}[\hat{{\beta}}]} = \frac{1}{N}\left(\frac{1}{N}\sum\mathbf{x}_{i}^{T}\mathbf{x}_{i}\right)^{-1}\left(\frac{1}{N}\sum\mathbf{x}_{i}^{T}\mathbf{x}_{i}\hat{\epsilon}^2_{i}\right)\left(\frac{1}{N}\sum\mathbf{x}_{i}^{T}\mathbf{x}_{i}\right)^{-1} \]

Homoskedasticity (\(\EE[\epsilon^2|\mathbf{x}]=\sigma_{\epsilon}^2\)):

\[\widehat{\BB{V}[\hat{{\beta}}]} = \frac{1}{N}\left(\frac{1}{N}\sum\mathbf{x}_{i}^{T}\mathbf{x}_{i}\right)^{-1}\sum\frac{1}{N}\hat{\epsilon}_{i}^2 = (\mathbf{X}^{T}\mathbf{X})^{-1}\mathbf{\hat{\epsilon}}^{T}\mathbf{\hat{\epsilon}} \]

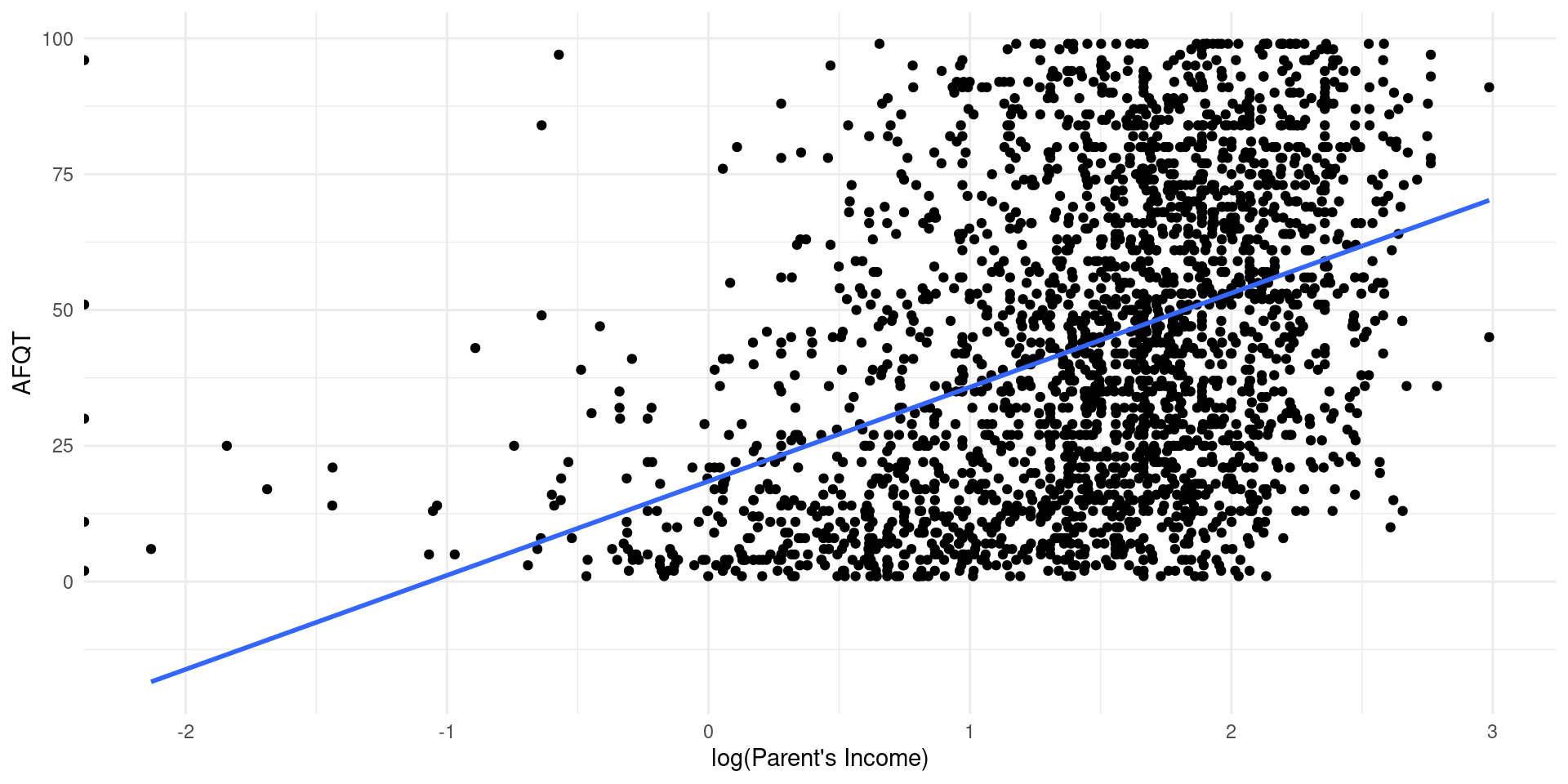

Non-robust:

Call:

lm(formula = afqtrev ~ log(mfinc1617), data = .)

Residuals:

Min 1Q Median 3Q Max

-54.42 -20.79 -2.43 19.32 88.43

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 18.4768 1.2319 15.0 <2e-16 ***

log(mfinc1617) 17.3188 0.7631 22.7 <2e-16 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 25.58 on 2479 degrees of freedom

Multiple R-squared: 0.172, Adjusted R-squared: 0.1717

F-statistic: 515.1 on 1 and 2479 DF, p-value: < 2.2e-16Robust:

Model: \[ \log(W_{i}) = \beta_{1} + \beta_{2}M_{i} + \beta_{3}F_{i} + \epsilon_{i} \] where \(M_{i}\in\{0,1\}\) indicates male and \(F_{i}\in\{0,1\}\) indicates female.

What’s wrong with this model?

The data:

| sex | occupation | age |

|---|---|---|

| Male | Clerical | 21-30 |

| Female | Manager | 31-40 |

| Female | Manual | 21-30 |

| Male | Manual | 41-50 |

The dummies

| sex | sex_Male | sex_Female |

|---|---|---|

| Male | 1 | 0 |

| Female | 0 | 1 |

| Female | 0 | 1 |

| Male | 1 | 0 |

| occupation | occupation_Clerical | occupation_Manager | occupation_Manual |

|---|---|---|---|

| Clerical | 1 | 0 | 0 |

| Manager | 0 | 1 | 0 |

| Manual | 0 | 0 | 1 |

| Manual | 0 | 0 | 1 |

| age | age_21-30 | age_31-40 | age_41-50 |

|---|---|---|---|

| 21-30 | 1 | 0 | 0 |

| 31-40 | 0 | 1 | 0 |

| 21-30 | 1 | 0 | 0 |

| 41-50 | 0 | 0 | 1 |

RAn example using wage data:

D <- read.csv("../data/cps-econ-4261.csv") %>%

filter(YEAR>=2011) %>%

mutate(EARNWEEK = na_if(EARNWEEK,9999.99),

UHRSWORKT = na_if(na_if(na_if(UHRSWORKT,999),997),0),

HOURWAGE = na_if(HOURWAGE,999.99),

OCCsimple = case_when(OCC<500 ~ "Managerial", OCC>=500 & OCC<6000 ~ "Other", OCC>6000 ~ "Manual"), #<- very broad and slightly wrong occupation codes

AGECAT = floor((AGE-1)/10)) %>% #<- create an age category

mutate(Wage = case_when(PAIDHOUR==1 ~ EARNWEEK/UHRSWORKT,PAIDHOUR==2 ~ HOURWAGE)) %>%

filter(!is.na(Wage),OCC>0,AGE>=21,AGE<=60) %>% #<- keep only people with non-missing wages and occupations, aged between 21 and 60

select(CPSIDP,AGECAT,OCCsimple,SEX,Wage)

knitr::kable(head(D))| CPSIDP | AGECAT | OCCsimple | SEX | Wage |

|---|---|---|---|---|

| 2.00912e+13 | 3 | Other | 2 | 12.00 |

| 2.00912e+13 | 3 | Manual | 1 | 14.50 |

| 2.01012e+13 | 3 | Manual | 1 | 16.50 |

| 2.01012e+13 | 3 | Other | 2 | 32.00 |

| 2.01012e+13 | 3 | Manual | 1 | 15.45 |

| 2.01012e+13 | 4 | Other | 1 | 24.05 |

Call:

lm(formula = log(Wage) ~ as.factor(SEX) + as.factor(OCCsimple) +

as.factor(AGECAT), data = D)

Residuals:

Min 1Q Median 3Q Max

-11.9217 -0.3495 -0.0166 0.3649 4.2964

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 3.312504 0.003752 882.86 <2e-16 ***

as.factor(SEX)2 -0.208918 0.002148 -97.27 <2e-16 ***

as.factor(OCCsimple)Manual -0.525808 0.003760 -139.84 <2e-16 ***

as.factor(OCCsimple)Other -0.313654 0.003272 -95.86 <2e-16 ***

as.factor(AGECAT)3 0.256600 0.002819 91.03 <2e-16 ***

as.factor(AGECAT)4 0.300951 0.002872 104.79 <2e-16 ***

as.factor(AGECAT)5 0.290471 0.002910 99.81 <2e-16 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.5758 on 328775 degrees of freedom

Multiple R-squared: 0.1141, Adjusted R-squared: 0.1141

F-statistic: 7056 on 6 and 328775 DF, p-value: < 2.2e-16Clean output by pre-defining factors.

Call:

lm(formula = log(Wage) ~ SEX + OCCsimple + AGECAT, data = D)

Residuals:

Min 1Q Median 3Q Max

-11.9217 -0.3495 -0.0166 0.3649 4.2964

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 3.312504 0.003752 882.86 <2e-16 ***

SEXFemale -0.208918 0.002148 -97.27 <2e-16 ***

OCCsimpleManual -0.525808 0.003760 -139.84 <2e-16 ***

OCCsimpleOther -0.313654 0.003272 -95.86 <2e-16 ***

AGECAT31-40 0.256600 0.002819 91.03 <2e-16 ***

AGECAT41-50 0.300951 0.002872 104.79 <2e-16 ***

AGECAT51-60 0.290471 0.002910 99.81 <2e-16 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.5758 on 328775 degrees of freedom

Multiple R-squared: 0.1141, Adjusted R-squared: 0.1141

F-statistic: 7056 on 6 and 328775 DF, p-value: < 2.2e-16

Call:

lm(formula = log(Wage) ~ 0 + SEX + OCCsimple + AGECAT, data = D)

Residuals:

Min 1Q Median 3Q Max

-11.9217 -0.3495 -0.0166 0.3649 4.2964

Coefficients:

Estimate Std. Error t value Pr(>|t|)

SEXMale 3.312504 0.003752 882.86 <2e-16 ***

SEXFemale 3.103586 0.003820 812.38 <2e-16 ***

OCCsimpleManual -0.525808 0.003760 -139.84 <2e-16 ***

OCCsimpleOther -0.313654 0.003272 -95.86 <2e-16 ***

AGECAT31-40 0.256600 0.002819 91.03 <2e-16 ***

AGECAT41-50 0.300951 0.002872 104.79 <2e-16 ***

AGECAT51-60 0.290471 0.002910 99.81 <2e-16 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.5758 on 328775 degrees of freedom

Multiple R-squared: 0.9668, Adjusted R-squared: 0.9668

F-statistic: 1.367e+06 on 7 and 328775 DF, p-value: < 2.2e-16

Call:

lm(formula = log(Wage) ~ 0 + OCCsimple + SEX + AGECAT, data = D)

Residuals:

Min 1Q Median 3Q Max

-11.9217 -0.3495 -0.0166 0.3649 4.2964

Coefficients:

Estimate Std. Error t value Pr(>|t|)

OCCsimpleManagerial 3.312504 0.003752 882.86 <2e-16 ***

OCCsimpleManual 2.786696 0.002815 989.99 <2e-16 ***

OCCsimpleOther 2.998850 0.002484 1207.41 <2e-16 ***

SEXFemale -0.208918 0.002148 -97.27 <2e-16 ***

AGECAT31-40 0.256600 0.002819 91.03 <2e-16 ***

AGECAT41-50 0.300951 0.002872 104.79 <2e-16 ***

AGECAT51-60 0.290471 0.002910 99.81 <2e-16 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.5758 on 328775 degrees of freedom

Multiple R-squared: 0.9668, Adjusted R-squared: 0.9668

F-statistic: 1.367e+06 on 7 and 328775 DF, p-value: < 2.2e-16d79 %>%

rbind(d97) %>%

filter(hhinccat==1 | hhinccat==4) %>%

lm(Dhgacoll2122 ~ 0 + as.factor(afqtq):(cohort*as.factor(hhinccat)),data=.) %>%

summary()

Call:

lm(formula = Dhgacoll2122 ~ 0 + as.factor(afqtq):(cohort * as.factor(hhinccat)),

data = .)

Residuals:

Min 1Q Median 3Q Max

-0.96519 -0.18855 0.03481 0.32161 0.84026

Coefficients:

Estimate Std. Error t value

as.factor(afqtq)1:cohort79 0.159744 0.022882 6.981

as.factor(afqtq)2:cohort79 0.397436 0.032411 12.262

as.factor(afqtq)3:cohort79 0.423529 0.043909 9.646

as.factor(afqtq)4:cohort79 0.733333 0.052262 14.032

as.factor(afqtq)1:cohort97 0.188552 0.023490 8.027

as.factor(afqtq)2:cohort97 0.401042 0.029215 13.727

as.factor(afqtq)3:cohort97 0.571429 0.036064 15.845

as.factor(afqtq)4:cohort97 0.790698 0.043652 18.113

as.factor(afqtq)1:as.factor(hhinccat)4 0.143827 0.058736 2.449

as.factor(afqtq)2:as.factor(hhinccat)4 0.002564 0.049754 0.052

as.factor(afqtq)3:as.factor(hhinccat)4 0.254863 0.052454 4.859

as.factor(afqtq)4:as.factor(hhinccat)4 0.190667 0.058196 3.276

as.factor(afqtq)1:cohort97:as.factor(hhinccat)4 0.146494 0.079434 1.844

as.factor(afqtq)2:cohort97:as.factor(hhinccat)4 0.237113 0.065653 3.612

as.factor(afqtq)3:cohort97:as.factor(hhinccat)4 0.035778 0.068981 0.519

as.factor(afqtq)4:cohort97:as.factor(hhinccat)4 -0.016174 0.076229 -0.212

Pr(>|t|)

as.factor(afqtq)1:cohort79 3.66e-12 ***

as.factor(afqtq)2:cohort79 < 2e-16 ***

as.factor(afqtq)3:cohort79 < 2e-16 ***

as.factor(afqtq)4:cohort79 < 2e-16 ***

as.factor(afqtq)1:cohort97 1.47e-15 ***

as.factor(afqtq)2:cohort97 < 2e-16 ***

as.factor(afqtq)3:cohort97 < 2e-16 ***

as.factor(afqtq)4:cohort97 < 2e-16 ***

as.factor(afqtq)1:as.factor(hhinccat)4 0.01440 *

as.factor(afqtq)2:as.factor(hhinccat)4 0.95890

as.factor(afqtq)3:as.factor(hhinccat)4 1.25e-06 ***

as.factor(afqtq)4:as.factor(hhinccat)4 0.00107 **

as.factor(afqtq)1:cohort97:as.factor(hhinccat)4 0.06526 .

as.factor(afqtq)2:cohort97:as.factor(hhinccat)4 0.00031 ***

as.factor(afqtq)3:cohort97:as.factor(hhinccat)4 0.60404

as.factor(afqtq)4:cohort97:as.factor(hhinccat)4 0.83198

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.4048 on 2705 degrees of freedom

(614 observations deleted due to missingness)

Multiple R-squared: 0.7122, Adjusted R-squared: 0.7104

F-statistic: 418.3 on 16 and 2705 DF, p-value: < 2.2e-16: and * in specificationd79 %>%

rbind(d97) %>%

lm(Dhgacoll2122 ~ 0 + as.factor(afqtq):(cohort*hhinccat),data=.) %>%

summary()

Call:

lm(formula = Dhgacoll2122 ~ 0 + as.factor(afqtq):(cohort * hhinccat),

data = .)

Residuals:

Min 1Q Median 3Q Max

-0.95689 -0.34255 0.08548 0.32329 0.84252

Coefficients:

Estimate Std. Error t value Pr(>|t|)

as.factor(afqtq)1:cohort79 0.125741 0.035273 3.565 0.000367 ***

as.factor(afqtq)2:cohort79 0.367893 0.041989 8.762 < 2e-16 ***

as.factor(afqtq)3:cohort79 0.333952 0.048407 6.899 5.85e-12 ***

as.factor(afqtq)4:cohort79 0.683555 0.053213 12.846 < 2e-16 ***

as.factor(afqtq)1:cohort97 0.072403 0.034848 2.078 0.037784 *

as.factor(afqtq)2:cohort97 0.336904 0.037585 8.964 < 2e-16 ***

as.factor(afqtq)3:cohort97 0.491145 0.042026 11.687 < 2e-16 ***

as.factor(afqtq)4:cohort97 0.738950 0.045892 16.102 < 2e-16 ***

as.factor(afqtq)1:hhinccat 0.031735 0.016935 1.874 0.060996 .

as.factor(afqtq)2:hhinccat -0.006814 0.016017 -0.425 0.670542

as.factor(afqtq)3:hhinccat 0.085690 0.016226 5.281 1.33e-07 ***

as.factor(afqtq)4:hhinccat 0.057740 0.016835 3.430 0.000609 ***

as.factor(afqtq)1:cohort97:hhinccat 0.058315 0.023164 2.517 0.011848 *

as.factor(afqtq)2:cohort97:hhinccat 0.088921 0.021262 4.182 2.93e-05 ***

as.factor(afqtq)3:cohort97:hhinccat 0.006719 0.021626 0.311 0.756055

as.factor(afqtq)4:cohort97:hhinccat -0.003255 0.022292 -0.146 0.883916

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.4195 on 5417 degrees of freedom

(2504 observations deleted due to missingness)

Multiple R-squared: 0.6887, Adjusted R-squared: 0.6878

F-statistic: 749.1 on 16 and 5417 DF, p-value: < 2.2e-16Specification from the paper: \[ Work_{itm} = \alpha + \beta 1_{im}\{day>10\} + \gamma FirstDay_{t} + \lambda 1_{im}\{day>10\}\times FirstDay_{t} + \nu_{i} + \mu_{m} + \epsilon_{itm} \]

From the paper:

We estimate this equation treating \(\nu_{i}\) and \(\mu_{m}\) as fixed effects or random effects.

What does this mean?

Fixed Effects:

fixest for convenient FERandom Effects:

\[ Y = 2 + 0.5X - c + \epsilon,\qquad X \sim \mc{N}(c-2,1)\]

OLS estimation, Dep. Var.: worked

Observations: 2,807

Standard-errors: Clustered (schid)

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.158416 0.038544 4.10997 0.00011647 ***

FirstDayTRUE 0.188119 0.054532 3.44967 0.00100655 **

inthemoney 0.523612 0.042631 12.28247 < 2.2e-16 ***

FirstDayTRUE:inthemoney -0.193247 0.059220 -3.26318 0.00178179 **

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

RMSE: 0.463745 Adj. R2: 0.055243d %>%

filter(t==-1 | t==1) %>%

feols(worked ~ FirstDay*inthemoney | schid + time,data=.) %>%

summary(vcov="iid")OLS estimation, Dep. Var.: worked

Observations: 2,807

Fixed-effects: schid: 64, time: 27

Standard-errors: IID

Estimate Std. Error t value Pr(>|t|)

FirstDayTRUE 0.121975 0.060723 2.00871 4.4667e-02 *

inthemoney 0.367959 0.046230 7.95933 2.5180e-15 ***

FirstDayTRUE:inthemoney -0.120609 0.063067 -1.91239 5.5932e-02 .

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

RMSE: 0.421323 Adj. R2: 0.19461

Within R2: 0.031146d %>%

mutate(First = t>0) %>%

feols(worked ~ First*inthemoney + First:poly(abs(t),3),cluster="schid",data=.) %>%

summary()OLS estimation, Dep. Var.: worked

Observations: 27,501

Standard-errors: Clustered (schid)

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.141982 0.024889 5.70459 3.3524e-07 ***

FirstTRUE 0.326991 0.039271 8.32658 9.5900e-12 ***

inthemoney 0.602585 0.025751 23.40034 < 2.2e-16 ***

FirstTRUE:inthemoney -0.334370 0.039360 -8.49512 4.8747e-12 ***

FirstFALSE:poly(abs(t), 3)1 2.200169 0.619532 3.55134 7.3176e-04 ***

FirstTRUE:poly(abs(t), 3)1 5.668366 0.524961 10.79769 5.7563e-16 ***

FirstFALSE:poly(abs(t), 3)2 -1.940820 0.592261 -3.27697 1.7092e-03 **

FirstTRUE:poly(abs(t), 3)2 -3.503322 0.575382 -6.08869 7.4959e-08 ***

FirstFALSE:poly(abs(t), 3)3 3.008277 0.426481 7.05372 1.6108e-09 ***

FirstTRUE:poly(abs(t), 3)3 -3.072773 0.534769 -5.74598 2.8560e-07 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

RMSE: 0.436042 Adj. R2: 0.079048d %>%

mutate(First = t>0) %>%

feols(worked ~ First*inthemoney + First:poly(abs(t),3) | schid + time,data=.) %>%

summary(vcov="iid")OLS estimation, Dep. Var.: worked

Observations: 27,501

Fixed-effects: schid: 64, time: 27

Standard-errors: IID

Estimate Std. Error t value Pr(>|t|)

FirstTRUE 0.290120 0.018564 15.62847 < 2.2e-16 ***

inthemoney 0.482583 0.014169 34.05955 < 2.2e-16 ***

FirstTRUE:inthemoney -0.297801 0.019305 -15.42614 < 2.2e-16 ***

FirstFALSE:poly(abs(t), 3)1 2.590093 0.600071 4.31631 1.5921e-05 ***

FirstTRUE:poly(abs(t), 3)1 5.640014 0.583933 9.65867 < 2.2e-16 ***

FirstFALSE:poly(abs(t), 3)2 -1.986118 0.598125 -3.32057 8.9950e-04 ***

FirstTRUE:poly(abs(t), 3)2 -3.507714 0.583831 -6.00810 1.9008e-09 ***

FirstFALSE:poly(abs(t), 3)3 2.836065 0.597929 4.74314 2.1149e-06 ***

FirstTRUE:poly(abs(t), 3)3 -3.082534 0.583915 -5.27908 1.3082e-07 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

RMSE: 0.416896 Adj. R2: 0.155411

Within R2: 0.05171